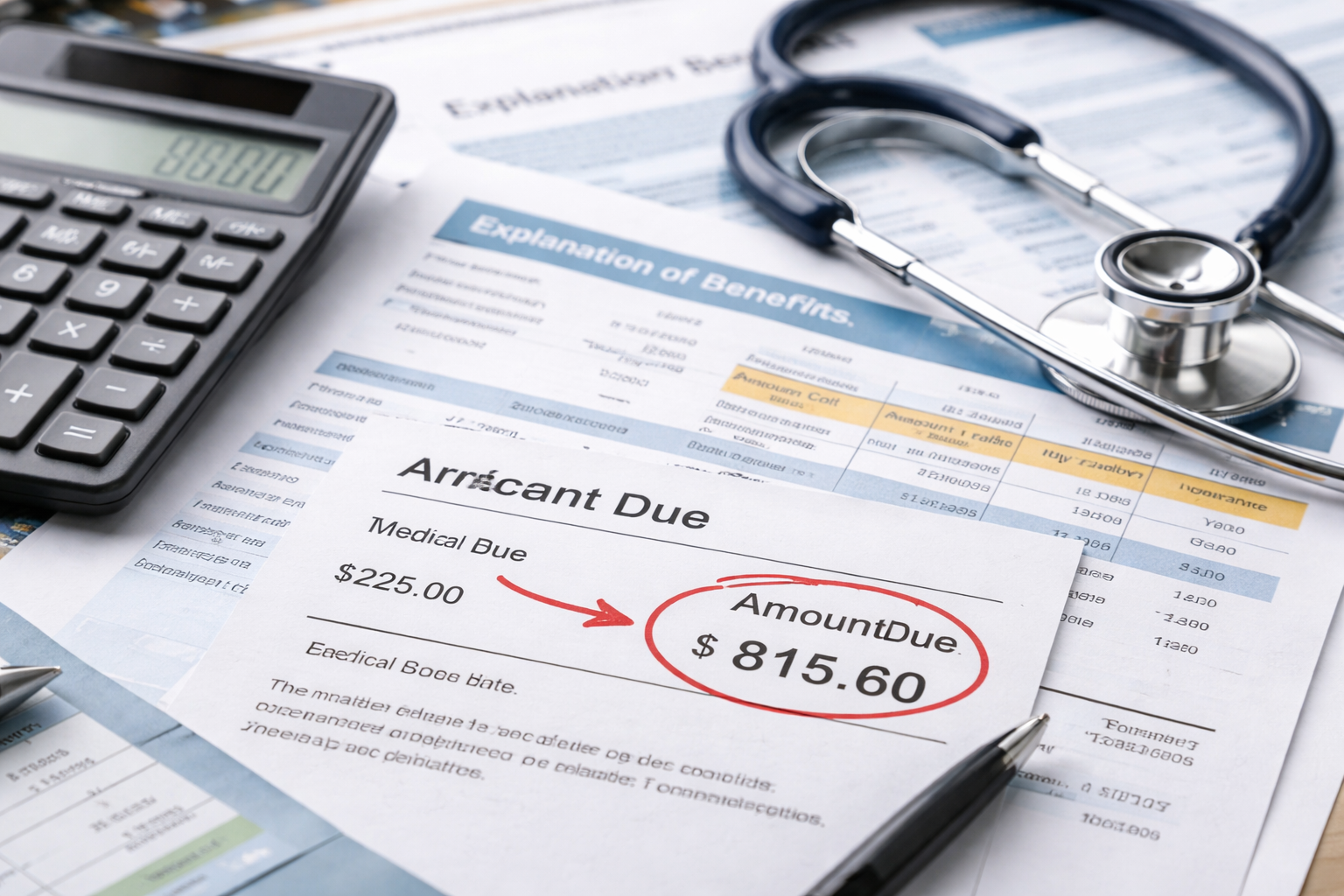

Medical bill increased after insurance adjustment was the exact thought that hit me when I opened a new statement and saw a larger balance than the one I had already been trying to deal with. The account had shown insurance activity before. There had been movement, an adjustment, and enough signs of progress that I assumed the visit was finally settling into its final amount. Then the next statement arrived and the number was worse. Not different in a small technical way. Worse in the kind of way that makes you reread the page three times because it feels impossible that a bill can go up after insurance already touched it.

What made it even more unsettling was how ordinary the statement looked. There was no large warning banner, no plain explanation, no sentence that said what had changed between the last version and this one. It was just a bigger patient balance, a due date, and the same polished layout that makes everything feel final whether it is correct or not. That is why this problem catches people off guard. When a medical bill increased after insurance adjustment, the danger is not just the higher amount. The danger is how easily that higher amount starts looking official before anyone has actually explained it.

If you want the broader framework for how billing mistakes usually start, spread, and get harder to unwind, begin here first.

Why a bill can go up after insurance touched it

Most people hear “insurance adjustment” and assume that means one thing: the charge was reduced and the account is moving toward closure. In real medical billing, that assumption can be wrong. An adjustment can mean a contractual write-off, but it can also mean a temporary posting, a corrected entry, a reversal, a claim reprocessing result, or a change in how patient responsibility is being allocated. That is why a medical bill went up after insurance even though the account appeared to be improving.

Sometimes the first version of the balance is built on incomplete information. The provider may have expected one insurer outcome and posted around that expectation. Later, the insurer finalized the claim differently. In other situations, the insurer did exactly what it meant to do, but the provider’s system posted the wrong follow-up balance or removed the wrong credit. In still other situations, more of the charge shifted into deductible, coinsurance, or a non-covered bucket after the claim was reviewed more carefully.

So when people ask why did my medical bill go up after insurance, the answer is usually not one simple explanation. It is usually the result of a later event in the claim trail or the provider ledger. The bill changed because something deeper changed first.

What actually changed behind the scenes

The patient sees a balance. The provider sees a ledger. The insurer sees claim adjudication logic. Those are three different views of the same encounter, and they do not always stay aligned. Medical bill increased after insurance adjustment often happens when one of those systems changes before the others catch up, or when the patient only receives the last version without seeing the adjustment trail that produced it.

Here are the most common background changes that cause this.

A reprocessed claim. The insurer may issue an initial result, then later revisit the same claim. That can happen after a coding review, eligibility correction, coordination-of-benefits update, duplicate review, medical necessity review, or network classification review. The new result may reduce insurer payment or change how much of the charge is assigned to the patient.

A reversed provider adjustment. A provider office may post what looks like a favorable adjustment early in the process, then later remove it when the final insurer result does not support that posting. From the patient’s point of view, it feels like the office took away money that had already been credited.

A shift into deductible or coinsurance. Insurance may have paid something and still left a larger patient balance than expected. That is one of the most common versions of insurance paid but I owe more medical bill. Coverage happened, but the portion insurance paid was smaller than the patient assumed when earlier account activity first appeared.

A network-status change. A service connected to an in-network facility may still process differently at the claim level if a radiologist, anesthesiologist, lab, assistant surgeon, pathologist, or other participant bills under different network terms. That is one way a hospital bill increased after insurance paid even though the visit initially looked straightforward.

A coding correction. The provider may have changed units, modifiers, or line-item structure. Sometimes those changes are proper. Sometimes they are not. Either way, the patient should not accept the larger number without seeing what exactly changed.

A split-account issue. One encounter can live in multiple account buckets. Facility charges, professional charges, lab charges, imaging charges, and follow-up charges may move on different timetables. One part gets adjusted while another part later increases, and the patient experiences it as one confusing bill.

Quick self-check before you start calling

- Did you receive a new EOB after the earlier one?

- Did a credit or adjustment disappear from the provider account?

- Did more of the balance move into deductible or coinsurance?

- Did any out-of-network wording appear later in the process?

- Did the provider submit a corrected claim?

- Did the balance rise even though you never got a clean explanation?

The most common balance increase patterns

The estimate pattern. The first patient balance was based on an estimate rather than a final insurer outcome. The provider system produced a statement too early, then the claim finalized later in a way that increased patient responsibility. This is common when the office moves quickly through statement cycles.

The partial-payment pattern. The insurer paid part of the claim, but less than the patient expected. This often creates the most confusion because the presence of insurance payment makes the larger balance feel impossible. In reality, the insurer may have paid one component while assigning more of the rest to deductible, coinsurance, or a non-covered category.

The removed-credit pattern. The account once showed a lower amount because a credit, write-off, or adjustment was posted too early or posted under the wrong assumption. When that entry gets removed, the new balance jumps. This is one of the most frustrating forms of medical bill increased after insurance adjustment because it feels like the account moved backward.

The corrected-claim pattern. The provider revised the claim after discovering missing modifiers, incorrect units, bundling issues, or documentation changes. The claim was resubmitted or corrected, and the patient responsibility changed with it.

The multi-entity pattern. One visit involved more than one billing entity, and the patient mistook the earlier statement as the entire financial picture. A later bill from the same encounter creates the impression that the original bill increased, when part of the change is actually tied to a different billing component. Even in that situation, the provider still needs to explain clearly what belongs to whom.

The review-and-reversal pattern. The account was touched by a later audit-style or compliance-style review. The initial claim result was not treated as final, and later internal review changed the financial allocation. When this happens, statements often lag behind explanations.

How provider answers and insurer answers stop matching

This problem becomes exhausting because the provider and insurer often sound like they are answering the same question when they are not. The insurer describes adjudication. The provider describes ledger activity. Both can give technically correct statements that still fail to explain the higher balance.

An insurer may say, “We processed the claim correctly.” That does not prove the provider posted the final patient balance correctly. A provider may say, “Insurance adjusted the claim.” That does not prove the insurer’s final EOB supports the way the provider calculated the new patient amount.

That is why broad questions usually fail. If you ask, “Why is my bill wrong?” you will probably get a generic answer. If you ask, “What exact ledger entry increased my patient responsibility from the prior statement?” you force the provider to identify a transaction. If you ask the insurer, “Was this claim reprocessed, and what changed from the prior EOB?” you force the insurer to identify a claim event.

Medical bill increased after insurance adjustment becomes easier to challenge when you stop arguing about the whole bill and start tracing the exact event that changed the number.

Detailed case branching you can match to your situation

If the insurer reprocessed the claim

This is one of the most important branches because the bill may have changed for a reason that never appeared on the provider statement in plain English. Ask whether there was a second adjudication date, a corrected EOB, new reason codes, or a revised allowed amount. Compare the earlier EOB to the later one line by line. If the insurer reduced the allowed amount or reassigned part of the visit to patient responsibility, ask why that happened and whether it involved network status, deductible, coordination of benefits, or coding review. Do not argue with the provider until you know whether the insurer actually changed the underlying claim result.

If the provider removed a previous credit

This branch matters when the earlier account balance looked manageable and then suddenly rose after a credit disappeared. Ask what kind of credit it was. Was it a contractual adjustment, a courtesy adjustment, an estimated insurance credit, a pending write-off, or a manual ledger entry? Ask on what date it was reversed and why. If the office cannot identify the type of credit that vanished, the account needs closer review before you treat the higher balance as final.

If deductible or coinsurance caused the jump

This is where many patients get trapped because the insurer did pay something, so the bill feels less disputable. But you still need to verify whether the deductible was open on the service date, whether another claim hit the deductible first, whether the coinsurance percentage was applied to the right allowed amount, and whether all related lines were processed consistently. Medical bill went up after insurance in this branch may be legitimate, but it still must be mathematically and contractually consistent with the EOB.

If out-of-network status appeared later

This branch needs extra attention because the patient often only learns about the network issue after the bill rises. Ask whether the increase involves the facility, the professional component, or an ancillary provider. Ask whether the service occurred in a setting where federal surprise-billing protections may apply. CMS explains those protections here: Know your rights under federal medical bill protections. Do not assume every out-of-network issue is prohibited, but do not assume the bill is valid either.

If one visit turned into several billing pieces

Ask the provider to separate facility charges, professional charges, lab charges, and imaging charges. Confirm whether the new amount belongs to the same billing entity or a different one. This branch is important because patients often think a previously known bill increased, when the system actually added a new but related component. That does not remove the need for clarity. It just changes what documents you need to gather.

If the account is close to collections

Speed matters more than perfection in this branch. Ask for a temporary hold while the bill is under review. State that the balance increased after insurance activity and that the amount remains disputed pending documentation. Keep copies of your dispute, the statement, and the EOB. A collections timeline should not move faster than the explanation of the charge itself.

If your situation involves a removed or reversed billing credit, this related article helps you separate a normal account update from a real reversal problem.

What rights matter here without overpromising

The safest approach is to avoid claiming that every higher medical bill is unlawful. Some higher bills are valid. But a valid increase still has to be explainable. You can request an itemized bill. You can request the provider’s transaction history or ledger notes to the extent they are available. You can compare the provider’s patient balance against the insurer’s final EOB. And in certain out-of-network situations, federal protections may apply depending on the service type and setting.

This matters because hospital bill increased after insurance paid is not always just a pricing problem. Sometimes it is a classification problem. Sometimes it is a timing problem. Sometimes it is a posting problem. Sometimes it is a network problem. You do not need to prove the whole healthcare finance system is wrong. You need to show that the higher amount is unexplained, unsupported, or inconsistent with the records.

What to do in the first hour

- Pull the newest EOB for the exact date of service.

- Pull the previous EOB too, if one exists.

- Pull the newest provider statement and the older one that showed the lower balance.

- Request an itemized bill.

- Request a transaction history or account ledger review.

- Write down the old balance, the new balance, and the date the change appeared.

- Ask the provider what exact entry raised the patient amount.

- Ask the insurer whether the claim was reprocessed and what changed.

- Save screenshots, PDFs, names, dates, and call reference numbers.

- If the account may move to collections, dispute in writing and ask for a hold.

Do not start by telling a long story. Start with the service date, the balance you saw before, the balance you see now, and the specific question you need answered. That structure gets better results because it forces the conversation around the actual change rather than your understandable frustration.

Mistakes that make the problem worse

The first mistake is paying the larger balance before understanding why it increased. The second is relying only on the provider portal summary. The third is throwing away older statements because they seemed outdated. The fourth is accepting a vague answer like “insurance reprocessed it” without asking what changed. The fifth is accepting “contact your provider” from the insurer without asking whether there is a newer EOB or revised claim result on file.

Another mistake is focusing only on whether the bill feels fair. Fairness matters, but billing disputes are usually resolved through traceable details. Medical bill increased after insurance adjustment is much easier to challenge when you can point to an earlier amount, a later amount, and the missing explanation in between.

If the account is already moving through a dispute pipeline or you need a clearer escalation path, this is the next article to read.

Key Takeaways

- Medical bill increased after insurance adjustment usually means the claim result or provider ledger changed after the earlier balance appeared.

- The most common causes are claim reprocessing, removed credits, deductible or coinsurance shifts, network-status review, corrected coding, or split-account billing.

- A later statement is not automatically the most reliable version of the account.

- The three most important documents are the updated EOB, the itemized bill, and the provider transaction history.

- If the account is approaching collections, move quickly and dispute before the timeline outruns the explanation.

FAQ

Can a medical bill really go up after insurance adjusts it?

Yes. Medical bill increased after insurance adjustment can happen when the insurer reprocesses the claim, the provider removes a prior credit, more of the amount is assigned to deductible or coinsurance, or a network or coding issue changes the patient responsibility.

Why did my medical bill go up after insurance if insurance already paid something?

Because insurer payment does not always mean the final patient amount was settled. Insurance may have paid part of the claim while leaving more responsibility to you than the earlier account activity suggested.

What if the provider says insurance changed it, but insurance says the claim was processed correctly?

Those answers can both be technically true. Ask the insurer whether there is a reprocessed EOB or revised adjudication, and ask the provider which exact ledger entry raised your balance. Usually the gap shows up there.

Should I pay first so the account does not get worse?

Usually that is not the best move when the increase is unexplained. It is safer to verify the basis for the higher amount before treating it as final, especially if the account changed after prior insurance activity.

What if I only have a summary statement?

Request an itemized bill and a transaction-history review. A summary statement is often too thin to explain why the balance increased.

What if this happened after I thought the issue was already resolved?

Then you should compare the earlier statement and any prior EOB to the newer versions immediately. A later increase often means a reversal, reprocessing event, or posting correction occurred after the earlier apparent resolution.

Medical bill increased after insurance adjustment is one of those problems that feels small until it starts moving faster than your ability to verify it. A higher balance becomes a due date. Then a collection risk. Then a paper trail you wish you had started earlier. That is why this is not just a billing annoyance. It is a documentation problem and a timing problem at the same time.

So do not wait for the next statement cycle. Pull the newest EOB, request the itemized bill, ask for the transaction history, compare the old balance to the new one, and make both the insurer and provider explain the same increase in concrete terms today. Do not let a larger number become your responsibility just because it showed up on newer paper with more confidence than explanation.